Inflation Today. Is it CPI or MyPI?

It’s easy to think of inflation as financial weather – something we must endure and can’t control. While it’s true we can’t individually control the prices that grocers, automakers and landlords charge, we can, and should, control what we spend.

We’re all familiar with the Consumer Price Index, or CPI. It tracks the cost of groceries, rent, utilities and other goods and services most of us use. When the cost of men’s sweaters go up, so does the index. CPI has been rising only very slowly recently, barely 2 percent a year.

But does the CPI reflect how you live and consume? Probably not. Like all statistical averages, it captures what’s typical for the masses, not what’s specific to you.

What really matters to you is the MyPI, the My Price Index.

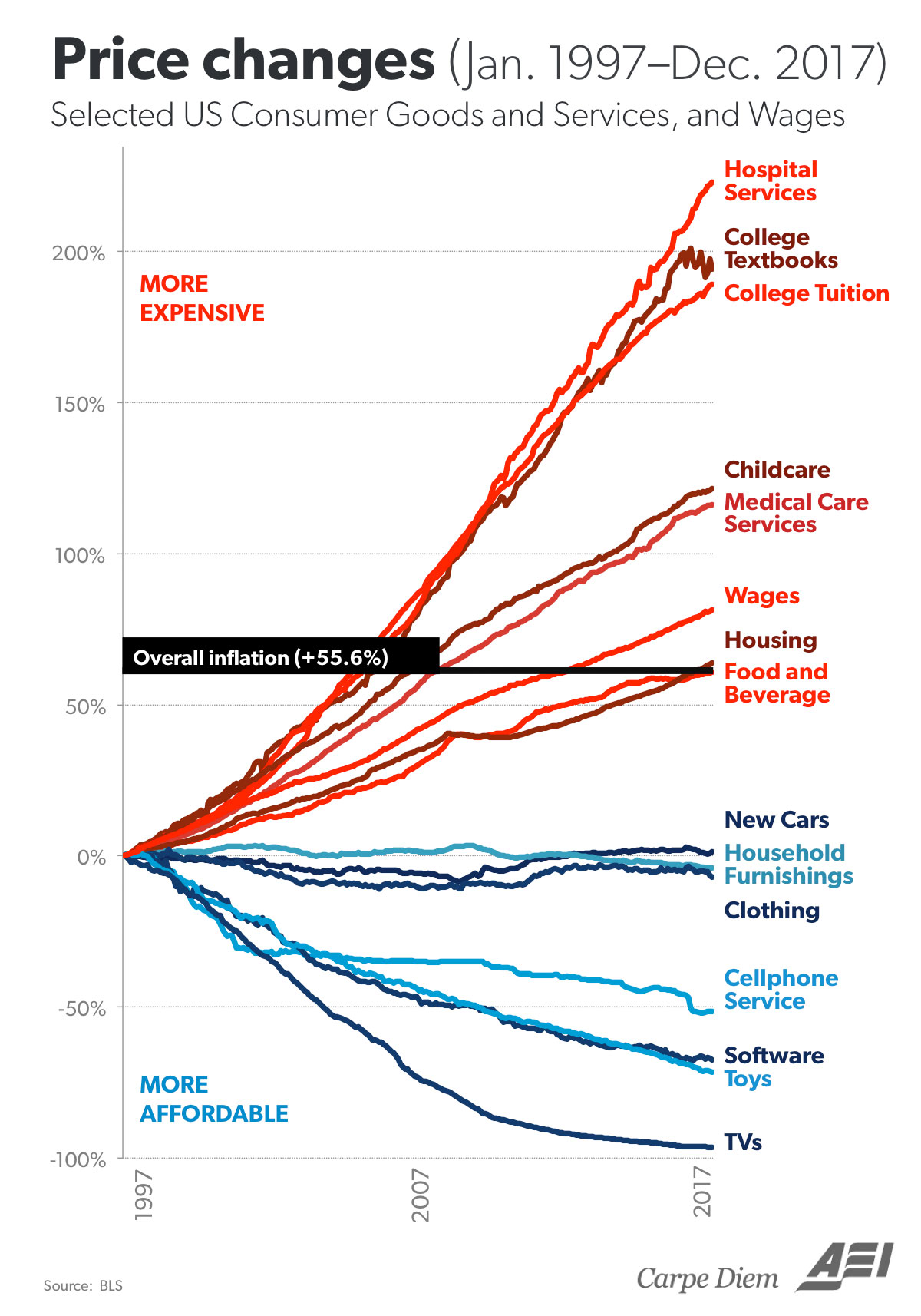

What you need vs what you want

Where do you fall on this chart? Are you spending in categories where prices are rising quickly, or is more of your money going to items with stable or falling prices? Is your vice a new car or TV every year? Do you tend to spend more on housing and renovations? Or does your kid’s education take the top seat on your annual expenses? Maybe you indulge in all categories because your income can support it. Many of the categories above have less expensive choices if you are willing to search for maximum value among alternatives. If you can squeeze out savings through thoughtful spending then you have more to invest and compound.

How high is high?

Bloomberg says that this week’s CPI number was at a six-year high of 2.8%. It also said the Fed’s separate, preferred inflation indicator is at 2%. Both numbers are only modestly higher from five years ago so the headlines are not really significant. But if inflation went to 4% quickly, that would be something noticeable. Four percent is what the bond market is worried about.

Your future, your choices

How will your spending change over time? Will your own cost of living hold fairly steady, or rise over the next 10, 20 or 30 years? Changing prices are part of the equation, but so are your own choices and behavior. Will slow and steady upgrades in your buying patterns raise your MyPI? Some refer to this as “lifestyle creep.”

Why do we care?

Your personal inflation rate over the next generation or so will have two big influences on your financial outcomes.

First, the higher your MyPI, the less your money can buy when you cash out of stocks and bonds. Put another way, MyPI is what your money needs to earn just to keep up with your spending habits. If your spending rises five percent each year, you need to earn five percent a year on investments just to hold your place in line.

Second, the inflation rate is the cost of holding cash. As we have discussed previously, anyone holding cash – often justifying doing so for its “safety” – loses purchasing power through the relentless erosion of inflation (see our calculator). We typically do not recommend holding cash for that exact reason (except in a short-term emergency fund). The higher your MyPI, the faster any cash holdings decline in value.

Take it personally

While low CPI growth has been a comfort over the last few years, we know higher inflation will return someday. Perhaps more importantly, we know that MyPI can surge at any time, thanks to our choices, priorities and tastes.

Weekly Articles by Osbon Capital Management:

"*" indicates required fields