Busting The Correlation Myth

When securities move in the same direction at the same time, that’s called correlation. If all stocks are highly correlated it doesn’t really matter what you own; all stocks rise or fall on the same fickle tide. “Everything moves together,” many complain. This is a common perception these days, but is it supported by the facts? Has too much correlation killed the markets?

In a word, I say no. You don’t have to search very far to find stocks that are not correlated. Just look at the Dow Jones Industrial Average. These 30 bellwether stocks are all large-cap domestic stocks, a group generally perceived to react more or less in lockstep to economic conditions and political developments.

But they don’t.

30 stocks, 30 stories

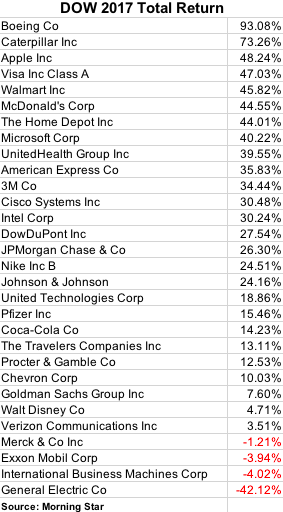

The chart below shows 2017 total return (price change plus dividend) for the Dow components. Twenty-six of the stocks had positive total returns for the year, four negative, with a range from +93 percent to -42 percent. That’s anything but lockstep.

Even during the 2008 financial crisis when all equities – large and small, domestic and international – seemed to plunge in horrifying harmony, some stocks lost far more than others, and some simply went to zero.

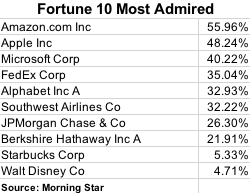

It’s the same story for Fortune’s 10 Most Admired Companies, shown below. While all shared the glow of customer admiration, the companies produced very different total returns in 2017, from 56 to 4 percent:

Each year, we also see significant disparities between asset classes. Non-correlation is not just a statistical phenomenon, it is the prime motivation for diversification – holding a variety of securities within an asset class to protect against big bad one-stock surprises like GE’s dismal 2017 performance. Non-correlation is also what makes asset allocation work – distributing money to asset classes with different performance characteristics to create an overall portfolio with the desired risk and return profile.

That’s why we diversify

Of course, we do see days when all stocks seem to move together, triggered by a major interest rate announcement, foreign economic crisis or other elephants in the room. But over time, correlations vary considerably. Some stocks win; others wallow. That’s one major reason why we strongly advocate diversifying. For example, ETFs can provide easy, low-expense exposure to dozens, hundreds or even thousands of securities within an asset class. This allows investors to earn market returns without overexposure to any single poisonous stock.

Weekly Articles by Osbon Capital Management:

"*" indicates required fields