Family Offices: A More Personal and Private Approach

Why are more wealthy families turning to family offices for investment management and wealth planning? At the top of the list are privacy, dedicated expertise and aligned incentives. A recent profile by The Economist on the family office landscape reveals interesting insights about how these offices are run, how they invest and why they appeal to more investors today. Here’s how you can follow along with the best of the industry:

What does the average family office look like?

Family offices are independently owned and operated, either by a single wealthy family or in the form of an RIA run for the benefit of a collection of families who share the combined cost of services and expertise. The average family office has 12 employees and serves assets ranging from $100 million to well over $1 billion. There are now 5,300 family offices worldwide with about two-thirds of those in Europe and America. For context, there are roughly 2,700 billionaire families globally.

Family office services range from the mundane to the knotty. In many ways, a family office acts as the CFO of a family, with goals that include keeping and growing wealth, assisting with trusts and estates, and even questions around prenups. Optimizing the transfer of wealth to the next generation is front and center in many family offices. Interestingly, that focus is often more on preparing the children for the money rather than the money for the children.

The opposite of banks

A big spark in the rise of family offices is the disillusionment with banks pushing their own products. Wealth attracts attention, much of it unwelcome, from the many product sales teams employed by banks. Wealthy families can use their family offices to screen out weak investment deals sold by pushy people. As an added layer of protection, family offices are required by law to meet the fiduciary standard – acting in the best interest of the client in all cases.

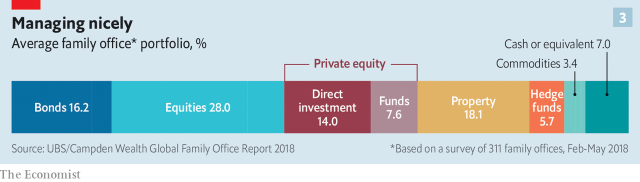

The average allocation of a family office

Diversification across appropriate types of bonds, stocks, real estate, private opportunities and cash is crucial to maintaining and growing wealth for the long run. This is especially true for family office clients who have access to more specialized investments than the average investor. Here’s what The Economist found about asset allocations among family offices:

Supplementing stocks, bonds and real estate, private investments make up just over 20% of the average allocation. The majority of those private investments are directly owned while investments in private fund’s accounts for only 7.6%. Private direct investments typically come from the close personal networks of each wealthy family.

Hedge funds continue to decline – now just 6% of the allocation. This is no surprise as many superstar hedge funds have recently kicked off the trend of converting their own funds into family offices for founders, employees and friends. Examples include Hightower, Leon Cooperman’s Omega, BlueCrest, and more.

The family office is in a golden age

Once serving only people named Rockefeller, Vanderbilt and Carnegie, family offices are now an option for a wider audience, providing better investment access, better technology, and access to large networks of expertise. More highly skilled professionals are opting for the family office structure because the incentives and long investment timelines better align client and advisor interests. If you’d like to learn more, just let us know.

Weekly Articles by Osbon Capital Management:

"*" indicates required fields