COVID-19 And The Weeks Ahead

Last week we experienced the first material market reaction to the Coronavirus, aka COVID-19. For months, prices had completely ignored any risks of the virus spreading until finally the news broke that it had reached the United States. This market reaction was a true black swan moment in that no experts or models could have adequately predicted it. Here’s a look at what has happened to date and what is likely to happen in the weeks ahead.

Unknowns and uncertainty

COVID-19 causes deep lung issues and has an expected incubation period of 3-14 days. A single infected person is expected to spread the disease to 3-4 people, that’s double the rate of the flu but significantly lower than other infectious diseases like measles (which has a transmission rate of ~12 people). Transmission is largely through droplets, like sneezes and coughs, which is why the CDC recommends that sick people wear masks, so that they contain their own droplet spread.

We know that many infected people never show any signs or symptoms. In that case, without knowing the total number of patients, we have almost no way of knowing the true mortality rate. Early mortality estimates range from 3.4% – 2%, and even as low as 1% (via Bill Gates).

The Last Worldwide Epidemic

The Spanish Flu epidemic erupted during 1918, towards the end of WWI. Due to the war, Governments tightly controlled the spread of information so the bulk of the virus press came from the one major nation that still maintained a free press. Spain. The virus ended up being significantly more deadly due to wartime censorship and poor quarantine policies.

Normally, healthy people will carry a strain of virus and continue on with their lives spreading their particular versions on to others. At the same time, people who are severely ill stay at home and limit the spread of their more vigorous strain. During Spanish Flu, this did not happen. Sick soldiers were sent out of the trenches via crowded trains into crowded hospitals. There was effectively no containment policy in place to keep the sickest of the sick separate from the rest. That allowed the worst strains to fester and eventually spread further via a deadly “2nd wave” of the virus.

Modern Medicine and Policy

In the near future, given the nature of the virus just about all of us will be exposed to a strain of COVID-19. It’s just a matter of time, now that we have growing numbers of cases on both coasts. If you want to see how the experts are reacting and planning ahead, I suggest reading Bill Gate’s post.

The Impact on Markets

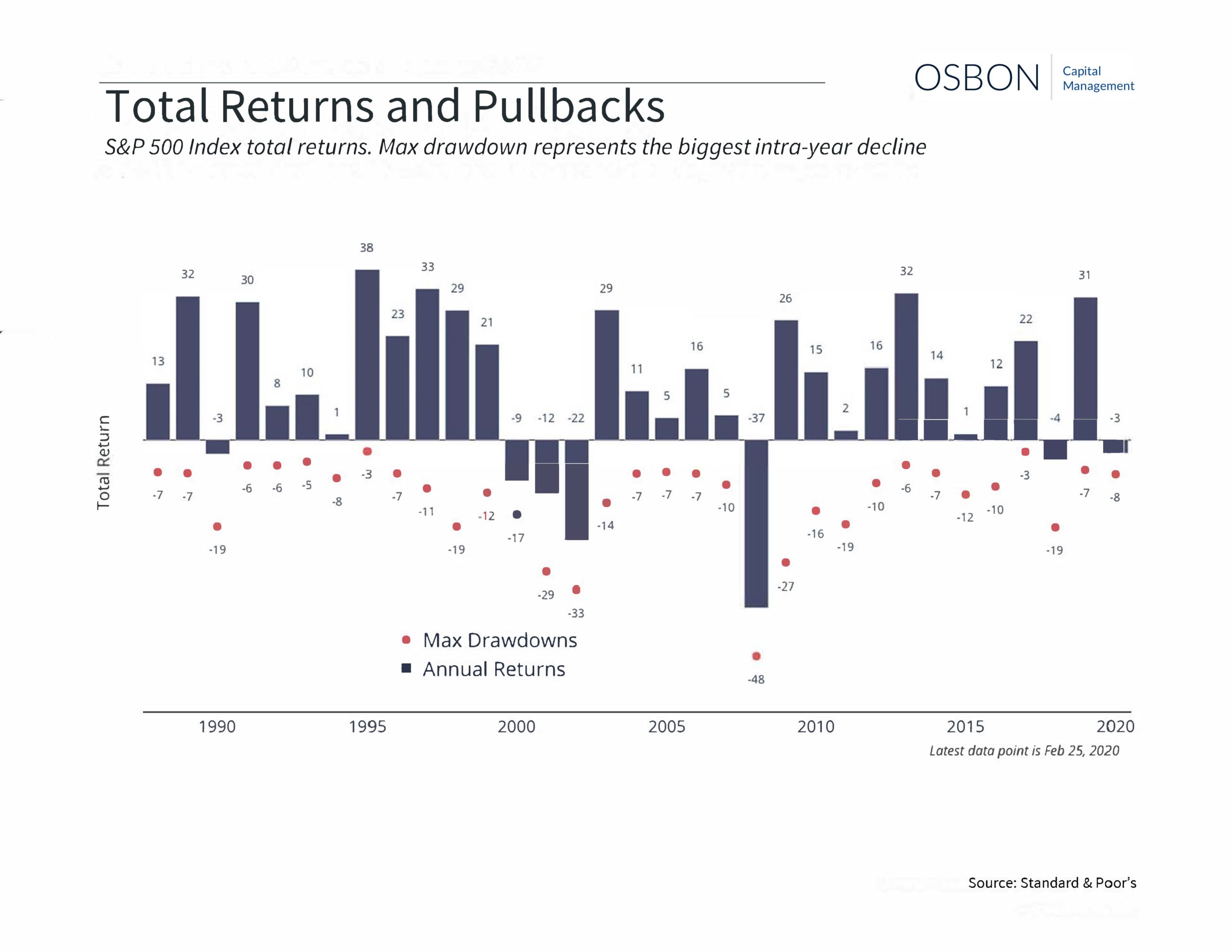

Global equities lost about 11% last week. While the drop was dramatic and much faster than normal, keep in mind that this puts us back to prices from October of 2019. Drawdowns of 10-20% in a calendar year are within the range of normal. What makes this particular drawdown different is the reason (viral epidemic) and the speed (panic) of the reaction. (See the chart at the end of this article.)

Typically we see market drawdowns tied to “unknown knowns”, like a particular default or earnings release. What we experienced last week was an intense market reaction to “unknown unknowns”, like questions surrounding mortality rates, speed of spread and other implications we typically don’t have to consider.

The pace of the rebound will depend on a handful of uncertainties. Supply chain disruptions appear significant, we don’t know how US consumer spending will react, and we don’t know how the mortality scenarios will evolve.

For those who are deeply interested, you can read the St. Louis Federal Reserve Study on the Economic Impact of the 1918 Spanish Influenza. There will be bouts of financial pain for the rest of the year, however, they will likely be short-lived once we learn more and witness the maturity of the coronavirus event over the next six months. Service and in-person entertainment will be hit hardest.

Corona Adjusted EBITDA

You can be sure that earnings numbers released in the next few quarters will heavily feature coronavirus discounting and distortion. Is a healthy company worth any less if their revenue was impacted for 18 months due to COVID-19? If they were significantly levered, then the answer is yes. High levels of debt turn bad situations into financial crises. Fortunately, debt levels for consumers and for most companies are at reasonable levels. There will be pockets of defaults, but the majority of businesses today are built to withstand some short term disruptions.

Diversification

In times like these, we are reminded of the role that fixed income plays in our portfolios. Treasuries remain a useful tool as yields continue to drop to previously unfathomable levels near 1%. For an investment strategy to work effectively, it must be able to withstand truly unexpected events. The question of, “how much fixed income should I have”, is entirely based on your current access to capital and the size and style of your future liabilities. We wrote about this recently in The Math Of Retirement.

Going Forward

We will continue to closely monitor risk levels and keep in mind any potential long term impacts. We don’t believe that it is possible to reliably predict when and by how much the entire global equity market will respond. As this event unfolds, there will be pockets of opportunity for clever and lucky investors. If you would like to express a view via a particular investment, please let us know and we will apply our experience. In the meantime, we are paying close attention to how further developments may impact markets.

Weekly Articles by Osbon Capital Management:

"*" indicates required fields